The COVID-19 pandemic. A new administration in the U.S. with, so far, a markedly different tone than the previous one. The MeToo and Black Lives Matter movements. Environmental, social and governance (ESG) reporting. It would be easy to attribute the emergence of human capital reporting requirement by the Securities and Exchange Commission (SEC) to a wave of accountability demands in a world rife with change. But for some organizations and investors, paying attention to human capital management is not new – they’ve been watching, measuring and reporting on people issues for some time, driven by a desire to be good corporate citizens, or invest in good corporate citizenship. The emergence of the SEC requirement, however, marks the beginning of a regulatory human capital trend we expect to evolve over time.

In August of 2020, the SEC announced amendments to disclosures under Regulation S-K, including ones that would require human capital reporting from public companies. The SEC’s increased focus on human capital disclosures has also led private, government and nonprofit organizations to consider human capital management practices in the interest of providing investors, donors, taxpayers, analysts and job candidates with greater transparency. Last month, we outlined steps to meet the new SEC requirement and explored how to measure the value of human capital in a substantive way. While financial returns and diversity statistics are important, human capital reporting is also about illuminating the intangible and central asset that the workforce represents. Beyond quantifying the value in financial terms, human capital reporting can showcase the ways leaders value the quality and caliber of their people.

Slow emergence from COVID-19 is driving new policies and protocols for business. Social movements are accelerating workplace conversations around diversity and inclusion. Leading organizations have begun collaborating on climate change initiatives and ESG reporting. All this creates a dynamic environment for the management of people. 2020 was an exceptional year, but change is always a constant. Human capital reporting provides an opportunity to explore how changes spurred by the pandemic and social movements influence organizations’ policies concerning people now and in years to come.

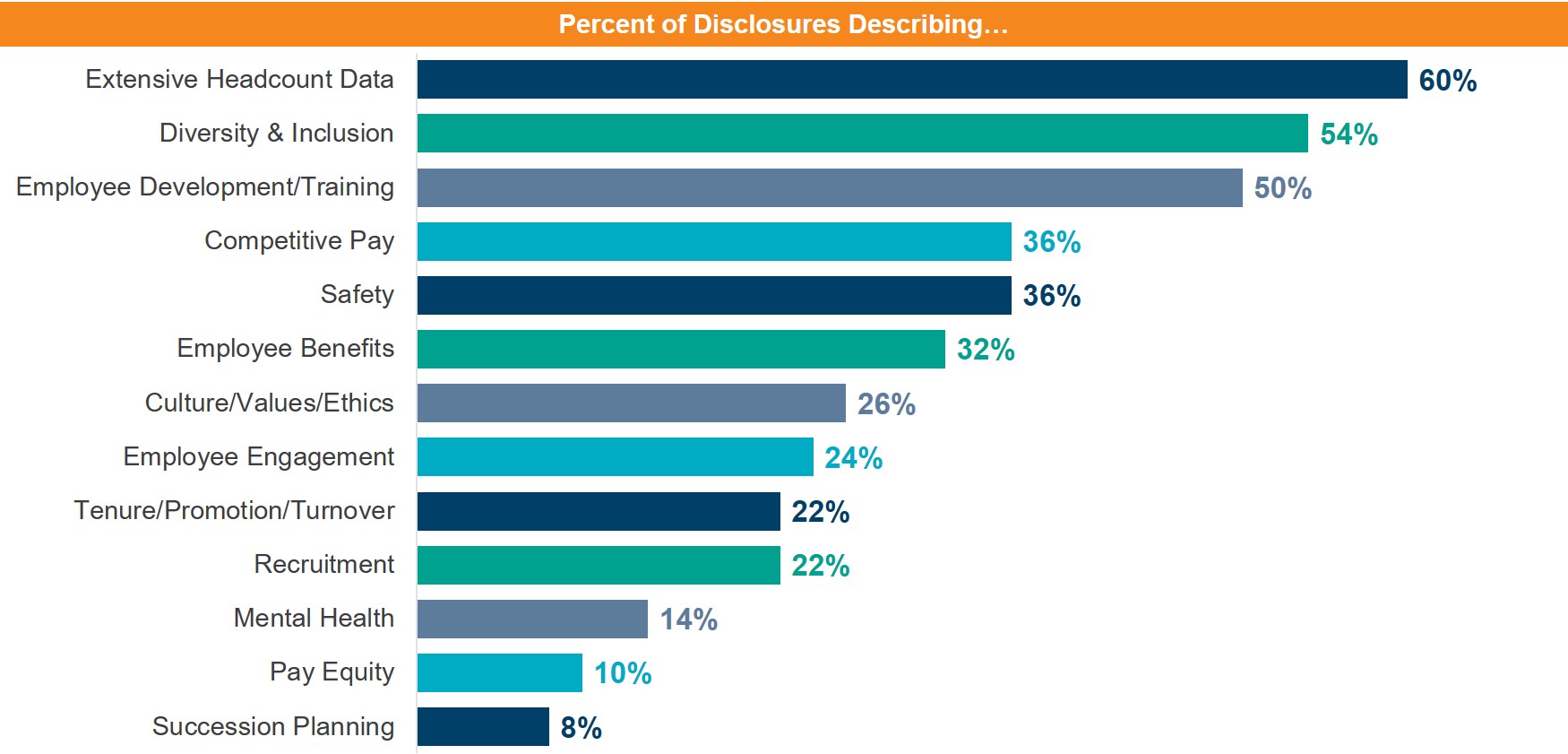

The SEC emphasized “a principles-based approach by requiring disclosure of information that is material to an understanding of the general development of a company’s business.” While the SEC hasn’t specified what facts to include, some common topics are emerging from reports filed already.

13 Common Disclosure Topics

Source: FW Cook, 2021.

Source: FW Cook, 2021.

The SEC’s new requirement leaves ample room for variation. We’ve observed a range of formats, depth and breadth of reports filed thus far. Consider two real-life examples (insurance companies):

- Firm A decided to meet the new requirement with a short brief with workforce data. They included two paragraphs of narrative about their employees and two tables of workforce diversity data that was independently verified by a third party.

- Firm B assembled a 55-page “fact book” that covered employee diversity, wellness, training, performance plans, career mobility, talent management and engagement. They’ve published this fact book in some form for at least ten years to demonstrate that their workforce is a competitive differentiator.

Firm A checked the box. However, the thoroughness of Firm B’s report conveys a meta-message: The firm is prepared to meet the SEC’s requirement and the intent of the regulation. They’re demonstrating competence in measuring, analyzing and monitoring the human capital domain, because they know that it matters as the ultimate indicator of how effectively they’re managing their principal asset and creating better shareholder returns.

Organizations that already monitor and report internally on people analytics are the first to possess the infrastructure and internal practices to succeed with external human capital reporting. Organizations that haven’t been reporting on human capital yet can start with a governance model that’s tied to strategy, then ensure that strategy cascades through all tiers of the organization. They can begin to monitor the performance of their reporting and policies routinely. Internal reports will provide the information that will enable leaders to manage metrics and demonstrate improvements year over year.

Telling a Story

Beyond presentation of metrics, the reporting process is also an opportunity to share an important narrative about the power of people. Leaders can articulate decisions they’ve made and help people outside the organization understand the rationales behind their choices. Over time, they’ll be able to show how their approach to human capital enhanced business performance. Collectively, a growing knowledge base of human capital reporting will demonstrate the effectiveness of policy decisions as businesses navigate a changing world. Organizations will be learning from one another’s leadership approaches in ways that weren’t possible before the availability of human capital disclosures.

How COVID-19 Is Changing Business

COVID-19 in particular has had a complex and momentous influence on people’s working lives. It generated fierce competition for talent in some fields, while others suffered and are facing a long recovery from the 2020 downturn. Meanwhile, employees have grown accustomed to working from home, and many now prefer to blend their work and personal lives.

Some organizations have discovered new opportunities in the midst of these changes. Two of remote work’s unintended consequences were flexibility and higher productivity. Projects that couldn’t easily be staffed onsite previously because of local talent shortage became feasible and profitable once the physical office location became irrelevant. Businesses could afford to initiate more costly projects after travel was removed from the budget and business conferencing and networking became virtual. International teams became commonplace and often brought global perspectives relevant to a global marketplace. And G&A costs took a dip.

The extent to which business customs will change to accommodate post-COVID concerns remains to be discovered. Human capital management considerations will define our new normal:

- Are employees ready to return to the office?

- Are they willing to travel on business?

- What are the impacts of the new normal on mental health?

- Should people be discouraged from shaking hands with customers?

Until or unless expectations revert to the standards from 2019 — when open-plan offices, frequent flying to meetings and shaking hands were customary — businesses can enjoy the few advantages that COVID has brought. As restrictions ease, leaders will need to reconsider their practices. They won’t all arrive at the same conclusions.

Looking Ahead

In the coming years, we expect the SEC to develop more specific human capital reporting requirements. We are already learning that the Sustainability Accounting Standards Board (SASB) is planning to issue more detailed guidance on human capital metrics similar to those for ESG reporting. We also expect organizations to leverage or invest in infrastructure and enhanced governance models to facilitate compliance as these requirements evolve. Lastly, we expect businesses to learn best practices for management from one another as conditions continue to change.

The movement toward measuring, analyzing, monitoring and reporting on human capital is a long-overdue acknowledgment of the value employees bring. Investments in reporting infrastructure are a must for organizations that want to realize the opportunity these new reporting requirements represent. Internal and external reporting can demonstrate management effectiveness and help leaders keep pace with competitors who are already excelling at their human capital management and reporting practices.

For more on this topic, watch our free on-demand webinar “Human Capital Reporting – Is Your Company Ready?”