- What happened – The European Parliament and the European Council have reached agreement on a proposal to delay certain adoption timelines of the Corporate Sustainability Reporting Directive (CSRD). The provisional agreement now only needs to be endorsed and formally adopted.

- Why it happened – Last September, EU Commission President Ursula von der Leyen pledged to reduce the reporting burden for companies by 25%. The adjustment of reporting deadlines is a fulfilment of that pledge. However, …

- … Read between the lines – On a practical level, the change in dates has very little impact for most companies, as we explain below. Despite media coverage of the announcement as a “relief,” the reality is more nuanced, and companies should continue their preparations without delay.

Go deeper.

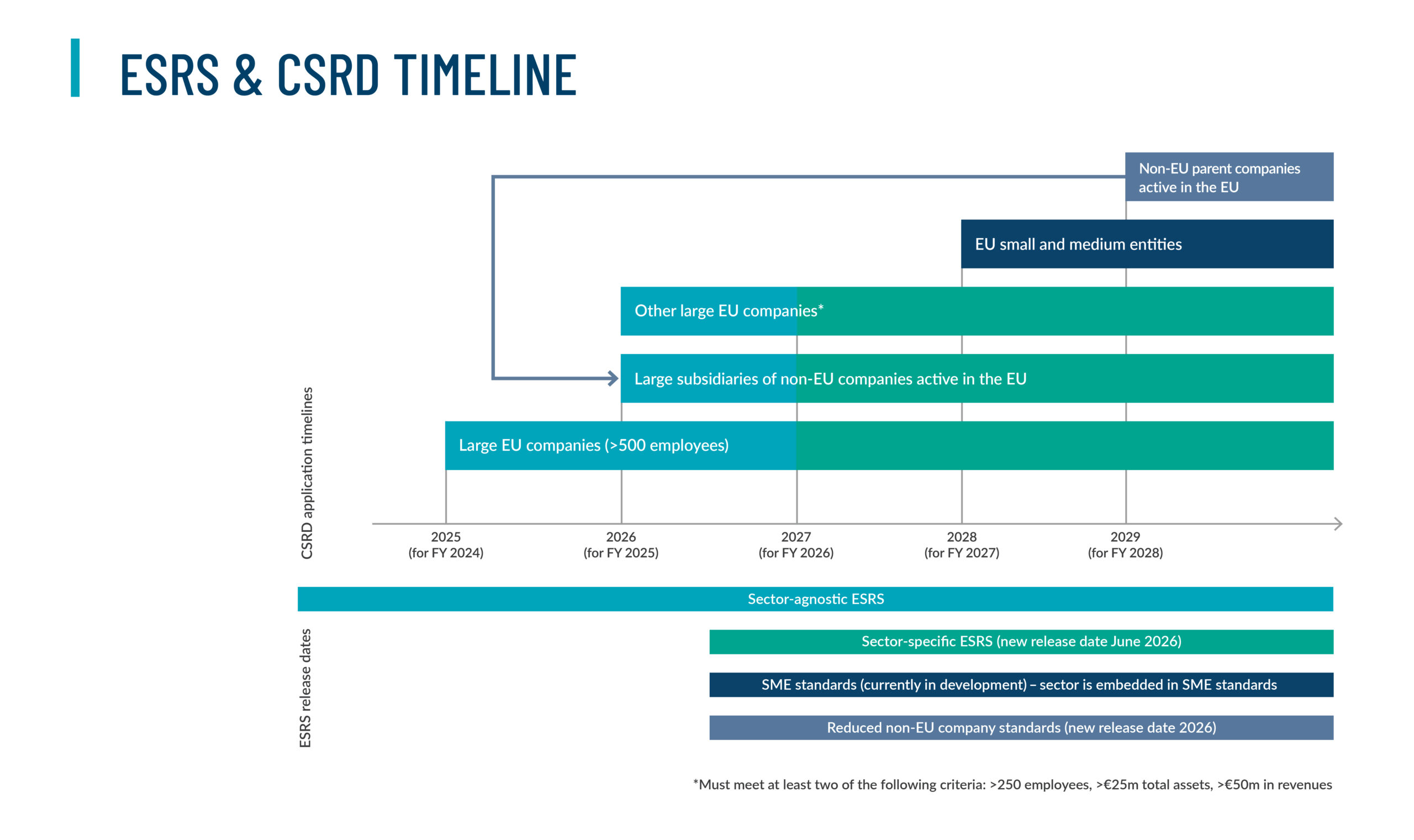

On 7 February 2024, the European Parliament and Council agreed to a proposal of the European Commission to delay certain adoption timelines of the CSRD by two years. Specifically, it agreed to the following changes:

- Sector-specific European Sustainability Reporting Standards (ESRS) – The release of these standards is delayed until 2026 (originally expected in 2024). However, EFRAG can release draft sector-specific standards earlier than 2026, as they are developed, and in this case, companies are expected to use the available standards if they apply to their sector.

- ESRS standards for non-EU parent companies with subsidiaries present in the EU (the so-called “reduced” standards) – These standards were expected in 2024 but will be released in 2026 instead. The companies to which they apply are expected to report using these standards in 2029 (for FY 2028). Note, however, that some EU subsidiaries of these companies may come in scope much earlier in 2026 (see graphic below), so the 2029 reporting deadline for their parents is not a notable relief.

Why is this news?

On a practical level, this isn’t news. The timeline for compliance remains largely the same. Large EU companies (“public interest entities” with > 500 employees) are already under obligation, and other large European companies (those that meet two of three criteria: > 250 employees, > €25m total assets and > €50m in revenues) and large EU subsidiaries of non-EU companies are coming right behind in 2026 — no change there. The current sector-agnostic standards are already a considerable effort, which was the main argument for why a delay in the sector-specific ones was needed. Almost all companies required to report in 2026 are busy preparing to meet their deadlines to avoid being completely overwhelmed once they reach the deadline.

The new release date for the sector-specific standards isn’t a significant event either, as every company reporting under the sector-agnostic ESRS (now or soon) will still have to consider entity-specific (and thus industry-specific) topics for their identification of material and relevant impacts, risks and opportunities. And individual draft sector-specific standards may be released earlier than 2026 at the discretion of EFRAG anyway, in which case organizations can start their preparations to use them earlier.

What about the 2029 deadline for non-EU companies?

2029 looks like a long time off on paper but consider this: Large EU subsidiaries of these companies need to report in 2026, using 2025 data. It would be more important for non-EU companies to check with their legal counsel whether they already fall within the scope in 2026 for certain subsidiaries than to presume they have been granted relief. While this reporting might be at the subsidiary’s level, input from the parent company will possibly be required.

Additional thoughts

It is worth considering the context in which these changes were approved. The reporting requirements of the CSRD proved so rigorous, as reported by the companies already in scope, that the EU commission realized more time for preparation really is warranted. Further, it became clear that companies needed more detailed guidance on the sector-agnostic ESRS (ESRS 1, ESRS 2, ESRS E1-E5, ESRS S1-S4, ESRS G1) before they even consider the sector-specific ones. The EU wanted to first focus on the general standards and provide more guidance, specifically on the value chain, double materiality assessment, etc., to support companies in scope. The voices from companies that are already working to capacity are coming loud and clear: “Take care of this as early as possible.”

Call to action…get started now

Our key message is, don’t be lulled into complacency by media coverage that makes it sound like the approved new deadlines give you more time. Follow developments closely and consult with your legal counsel on specific timelines, scopes and standards. The existing requirements are already so difficult that putting certain priorities on the back burner for now was warranted — but the burden has not diminished. Get started now.

For more information, see this blog for recommended actions and areas of focus.